30th January 2018: Today we launch our fifth annual review of the European power sector – and for the third year in a row with Agora Energiewende. The 5 key findings from the report are summarised below, but please download the report for the full picture, pieced together from a variety of European and national data sets.

Europe’s coal phase-out is gathering pace as renewables continue to grow. EU total coal generation fell by 6 percent in 2018 and was 30 percent below 2012’s generation. But it’s a tale of two types of coal: most of the fall has been from hard coal, and not dirtier lignite. Europe’s phase-out of hard coal is gathering pace, but Europe’s phase-out of lignite is only just beginning.

Download the Full Report (PDF, 2.2MB)

Download the data

(Excel, 0.5MB)

“Europe is proving that replacing coal generation with renewable generation is the fastest way to cut emissions. In just six years, between 2012 and 2018, Europe’s annual CO2 emissions from coal power plants have fallen by 250 million tonnes with no increase in emissions from power generation with natural gas. But it’s a tale of two coals: most of the fall is from hard coal, and not dirtier lignite. Europe’s phase-out of hard coal is gathering pace, but Europe’s phase-out of lignite is only just beginning.”

Dave Jones“The EU so far largely missed the opportunity to profit from the very favourable solar module prices, which mean that solar power from new plants is now often cheaper than electricity from conventional power plants. On the positive side, however, three countries – Spain, France and Italy – are now aiming for solar outputs of 45 gigawatts and more. This makes the potential very clear and will set an example.”

Matthias Buck1) CO₂ emissions in the power sector fell by 5% in 2018

Half of this was structural, from new wind, solar and biomass displacing hard coal. The other half was weather-related, as increased hydro generation reversed the temporary rise in gas in 2017.

Overall EU ETS emissions, we estimate, fell by 3%, from 1754 Mt in 2017 to 1700 Mt in 2018.

From 2012 to 2018, most of the falls in EUETS emissions have been from hard coal power plants. Hard coal power plant emissions have fallen by 41%. Lignite emissions meanwhile fell by a more mediocre 13%. Gas power plant emissions are near-flat – showing there gas is not increasing as coal is falling. The most disappointing is industrial emissions, which are expected to be exactly unchanged since 2012.

This report gives proof that the biggest falls in coal generation is in countries that have built the most renewables; and the smallest falls in coal generation is in countries that have built the least renewables.

EU ETS emissions split by sector:

2) Europe’s transition from hard coal to renewables is accelerating …

Hard coal generation fell by 9% in 2018, and is now 40% lower than in 2012.

In 2018, Germany and Spain announced that coal phase-out plans were imminent. That would now put three quarters of Europe’s 2018 hard coal generation under national coal phase-outs. Where date have been agreed, they are all for 2030 or earlier. Spain’s date is under discussion. Germany’s coal commission has proposed 2038.

The remaining quarter of hard coal generation in 2018 is almost all in Poland.

EU hard coal generation:

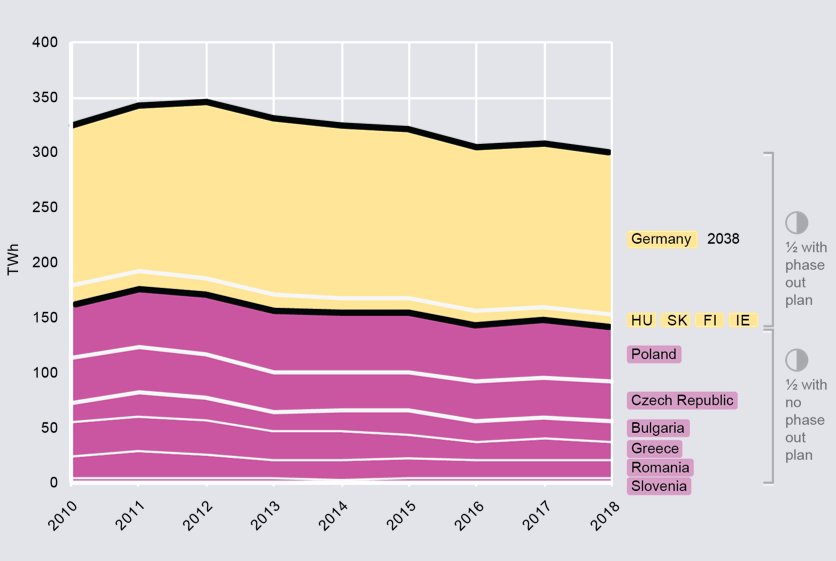

3) …however, the transition from lignite to renewables is proving much harder.

Power generation from lignite (the dirtier, brown coal) fell by only 3% in 2018.

Half of Europe’s lignite generation in 2018 was in Germany; the Coal Commission announcement for a 2038 phase-out includes lignite. The Coal Commission’s plan indicates more hard coal plants will close than lignite by 2022 and by 2030, suggesting that Germany’s phase-out will be faster for hard coal and slower for lignite.

The other half of 2018 lignite generation was in six countries where discussions have yet to bear fruit: Poland, Czech Republic, Bulgaria, Greece, Romania and Slovenia. These countries are not only slow to discuss their lignite transition, but they also have very unambitious plans for future wind and solar expansion so far. We hope their national climate plans will unveil a new ambition.

EU lignite generation:

4) Get ready for solar!

Renewables rose to 32.3% of EU electricity production in 2018. This year’s rise was mainly due to wind growth picking up and hydro returning back to normal. Solar was only 4% of the electricity mix in 2018, way below wind and biomass, but developments in 2018 make us sure solar will be the next big thing.

Solar additions increased by more than 60% to almost 10 GW in 2018 and could triple to 30 GW by 2022. Module prices fell by 29% in 2018. Solar outperformed during the 2018 summer heatwave, when coal, nuclear, wind and hydro all stumbled. Bold national plans for solar in 2030 were drafted in Italy, France and Spain in 2018. The EU’s 2030 RES target, agreed in 2018, will result in even more.

EU solar installations:

5) Wind and solar are – for the first time – on a par with costs for existing coal and gas plants.

Coal and gas generation costs rose in 2018: coal price rose 15%, gas rose 30%, and the CO₂ price rose 170%. Consequently, electricity prices rose to 45–60 €/MWh in Europe. This is the level at which the latest wind and solar auctions cleared in Germany.

Coal and gas costs, versus German wind and solar auction prices: