The deadline for UK coal phaseout is looming and the remaining 6GW of coal capacity on the grid must be replaced. Meanwhile, options for cutting emissions from the heat (gas) network have yet to make significant progress. In response to the National Infrastructure Commission’s (NIC) technology study, which closed for evidence on Wednesday 15th March, Sandbag called for a step change in support for low-carbon infrastructure and investment in a the UK’s energy storage industry, and a new strategy for kick-starting the hydrogen economy.

In February the National Infrastructure Commission, a group of experts advising the government, launched a call for evidence on the technology and infrastructure the UK needs in the coming decades. Sandbag’s responses highlighted three technologies available in the short term to take the next steps in building low-carbon heat, power and industrial infrastructure in the UK:

- Energy storage, particularly lithium-ion batteries, to replace fossil capacity

- Hydrogen & CCS hubs to replace natural gas (methane) for heat

- Carbon Capture and Storage (CCS) to attract low-carbon industry

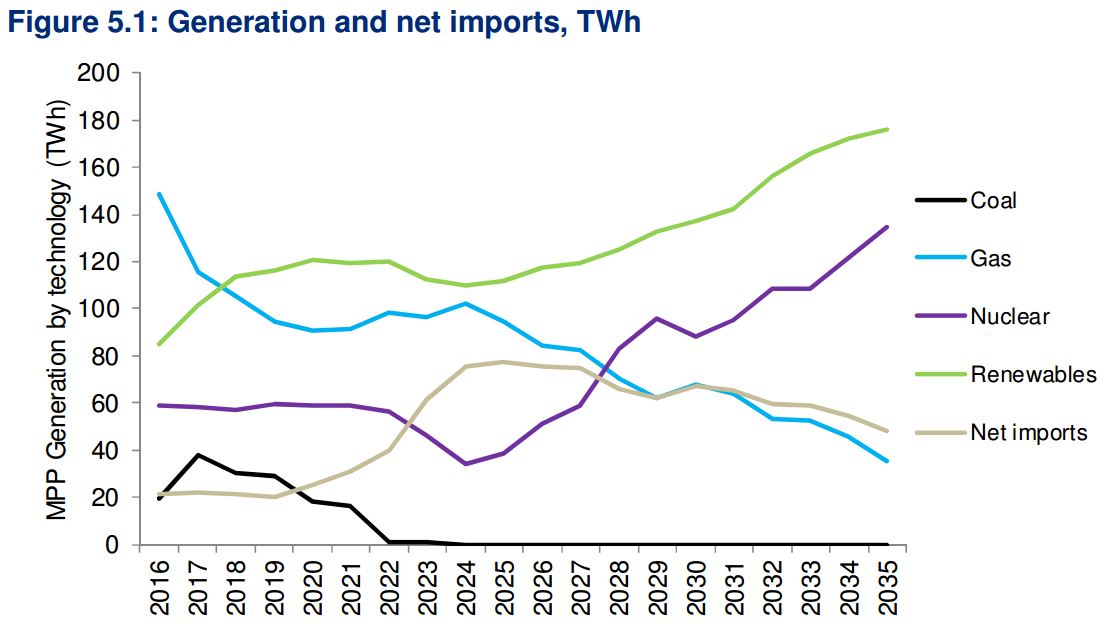

Electricity generation projections for 2035, from the BEIS March 2017 update. An increase in renewables will require a smarter grid with energy storage

The technologies highlighted in Sandbag’s responses were, until recently, prohibitively expensive and lacked a clear strategy for future development. The situation has now changed as these technologies are nearing cost parity with traditional forms of energy generation. Each in turn can be used to decarbonise electricity, heat and industrial processes.

Can battery connections increase rapidly enough to meet the 2023 capacity gap?

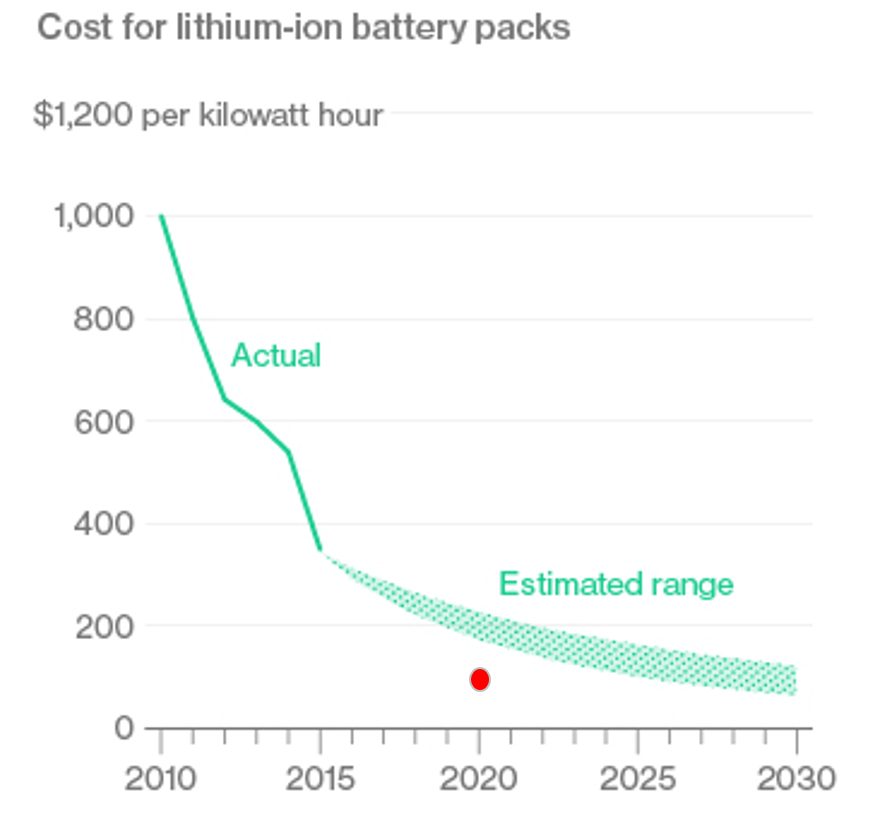

Lithium-ion battery technology is following the cost-curve of solar PV and wind, with price falls repeatedly outpacing analysts’ predictions. As the UK replaces cheap, polluting (and often unreliable) coal capacity with clean but intermittent renewable generation, the evolving grid requires energy storage capacity to act as a buffer during peak demand.

The UK market has shown strong appetite for energy storage, as evidenced by successful bids for 500MW of battery storage in the capacity market auction and the Treasury throwing its weight behind electric vehicles. In Europe, plans are afoot to manufacture batteries for storage on an unprecedented scale. Growth of commercial scale storage is also being driven by opportunities for price arbitrage between peak and off-peak hours.

Battery price costs and predictions from Bloomberg New Energy Finance (2016 prices and Tesla’s 2020 price expectation are already below the estimated range)

Can we begin the transition to a low-carbon heat network by blending hydrogen into the gas networks?

Sandbag’s immediate vision is to create four hydrogen supply hubs on the east coast of England, at each of England’s major North Sea natural gas terminals. New hydrogen capacity, produced in Steam Methane Reformers, can immediately be blended into the UK’s natural gas network at rates of up to 20%, creating opportunities for higher value, innovative hydrogen-based transport and electricity projects. CO2 from Steam Methane Reformers can be relatively easily captured, and Norway has offered to begin shipping CO2 out to be stored in the Norwegian North Sea. The projects can begin to cut emissions from the heat network almost immediately.

In time, the hubs would enable full decarbonisation of the gas heat network (the only alternative route is electrification of heating). Carbon Capture and Storage would move from ships to UK pipelines, opening up avenues for other industries to store their emissions. Innovation in fuel cells and hydrogen-fuelled vehicles will also create export opportunities for businesses that tap into these hubs.

A steam methane reformer at the Port Arthur 2 plant, Texas (Image from US Department of Energy)

Can we build low-carbon industrial hubs with Carbon Capture and Storage?

By 2050, industry will need to produce net zero or even negative carbon emissions. This is an enormous challenge given that CO2 emissions are inherent to many industrial processes. To maintain industrial productivity in carbon-intensive sectors such as steel and cement, their process emissions will therefore have to be captured at source and permanently stored.

Sandbag’s vision for the UK is to create the first integrated Carbon Capture and Storage (CCS) infrastructure hub, producing zero-carbon cement, steel, and other conventionally high-emitting industrial products, with technology that is cost-competitive with other construction materials. This has real synergy with the beginning of CCS at the UK’s new hydrogen hubs.

There is significant potential for CO2 storage in decommissioned North Sea oil and gas infrastructure. Furthermore, CCS supports the production of low-carbon hydrogen for decarbonising the heat and transport networks.

To meet emissions targets cost-effectively, the UK must invest strategically in technologies that reduce hurdles for industry and consumers to cut emissions. Doing so will provide additional benefits in the form of increased skilled employment, higher industrial productivity and opportunities for the UK to export expertise and products overseas. Energy storage with hydrogen and CCS infrastructure can revolutionise UK industry, and deliver the necessary full decarbonisation of the heat and electricity networks

Recent Comments